1st Quarter 2026

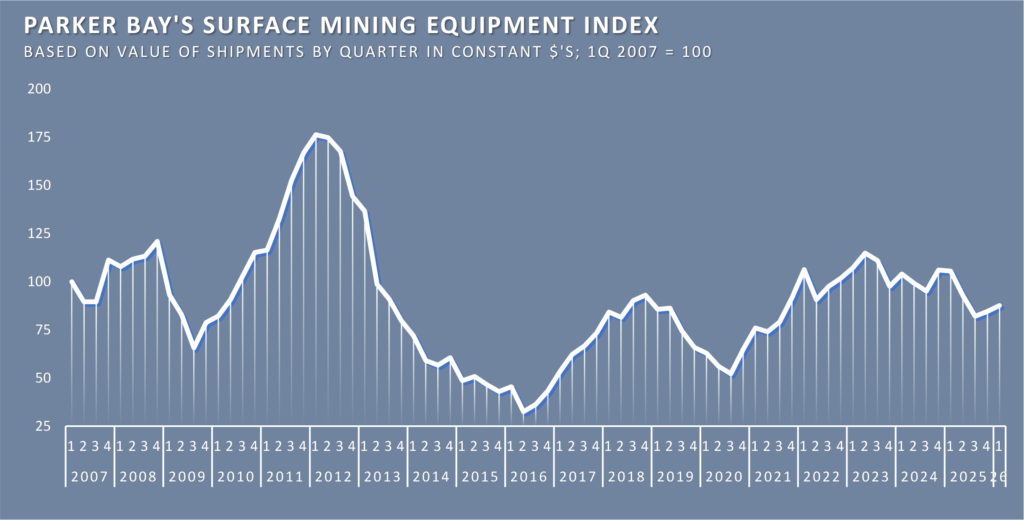

Units shipped during Q1 were lower by three percent vs Q4 but were 3.6% higher in valuation. Reflecting this, Parker Bay’s Mining Equipment Index rose for the second time from to 82.1 in Q3 2025 to 87.5 in Q1. However, this modest increase compares to the 22% decline between first and third quarters of last year. Thus, the recent gains may not indicate a significant market turn unless confirmed by stronger positive increases in shipments throughout 2026.

For the global market by product line, the value of shipments diverged appreciably. The aggregate value of truck shipments, which account for two-thirds of the total, increased by 6.4% in value. Hydraulic shovels/excavators increased by 34%, more than offsetting the decline during Q4. The valuation of wheel loaders shipped increased by nearly 20% but remained well below the last cyclical peak. In sharp contrast, crawler and wheel dozers delivered declined by 30% though this follows a relatively strong Q4.

There were significant variations in shipments by geographic regions as is common over short periods. Deliveries to mines in Asia increased by 22% but these shipments accounted for less that 10% of the global total in Q1. Australasia, which accounts for nearly one fourth of worldwide shipments, increased by 7%, and Latin America by 9%. In sharp contrast, North American deliveries were down 16%. Russia/CIS continued to recover from sharp declines that began in late-2023 likely due in part to the impact of the war with Ukraine. Nevertheless, the region’s shipments remain a third or more below those of 2022-23.

The distribution of shipments by mineral sectors shows some anomalous shifts. Coal mines worldwide received 37% more machines than in Q4. But this total is less than half the average quarterly shipments to coal during 2022-2023, illustrating the long-term secular decline. Metal mines worldwide vary greatly: copper was up 20% while gold and iron mines received modestly lower shipments. For gold mines, this contrasts with the very strong pricing and may simply reflect delays in bringing new capacity online. Shipments to oil sands were down slightly. The impact of sharply higher oil prices brought on by the war in Iran has not filtered through to this sector and may be reflected during the second half of the year if oil prices are sustained, and Canadian mines step up output to replace other oil production declines.

Explanation of how the Index is Developed The PBCo Mining Equipment Index is a measure of the quarterly evolution of surface mining equipment shipments worldwide. It relies on data from Parker Bay’s Mobile Mining Equipment Database and encompasses the same product range covered by the Database*. The index utilizes the value of equipment as opposed to number of units such that one $10mm excavator has the same weight as five $2mm trucks. Values are not based on the price of each unit as sold but instead an approximate value assigned to machines by size class and product expressed in constant $’s (updated annually). As such, the index does not reflect changes in equipment pricing but rather the overall sales volume. The base for the index is Q1 2007=100. Quarterly figures are not seasonally adjusted. *All products are included except draglines whose low volume, high $ value, long lead time sales can cause fluctuations that don’t reflect the quarterly changes in the market.

Shipments during Q4 were up over Q3 by 7.8% for units and just 4.8% for aggregate valuation across all products. Reflecting this, Parker Bay’s Mining Equipment Index rose from 82.4 to 86.4. But on a year-over-year basis (Q4 2025 vs Q4 2024), deliveries declined by over18% indicating that the Q4 increase may not indicate a significant market turn unless confirmed by stronger positive increases in shipments in 2026.

Looking at the annual figures, for the global market for all products we cover, unit shipments declined by 6% and the value of these deliveries by 9% for 2025 compared to 2024. The decline in volume was matched between trucks and excavators/loaders. But the value of these shipments diverged appreciably with aggregate value of truck shipments down 7% while the value of excavators/loaders declined by 17%. The difference is largely due to a global shift toward smaller capacity hydraulic shovels and wheel loaders. The significance of this change requires a more in-depth analysis.

Across the full year, the value of deliveries to Africa and Latin America increase by 14% and 13% respectively, more than offset by declines of 24% to mines in North America and 26% to those in Russia/CIS. In between, shipments to the largest geographic sector, Australasia, declined by 12%. Deliveries last year reflect a sharp divergence between metal markets and coal. The latter continued a secular decline with deliveries off 36% vs 2024. Metal mines did reduce their acquisitions of these machines in 2025 but to a much lesser extent. Collectively shipments to copper, gold and iron mines worldwide declined by 13%. But despite strong underlying fundamentals, gold mine purchases were down by 22%, compared to 9% each for copper and iron. As with changes among products and between regions, more in-depth analyses is required to determine why, and if these are short-term shifts or more significant secular developments.

Following the sharp downturn in Q2 shipments (11% lower than Q1 by value), we questioned the longevity of the Q2 decline indicating it might not represent a long-term shift in miners’ equipment requirements, to wit “since equipment shipments are the end result of longer-term capital investment decisions followed by months-long purchasing decisions and subsequent manufacturing schedules, it seems unlikely that the decline in Q2 shipments resulted from the greater global market uncertainty that is impacting other economic sectors.”

But the Q2 decline was followed by a comparable reduction in Q3 deliveries: 12% by volume and 13% by value. However one defines a business cycle in the global mining equipment market, Parker Bay considers the combined 25%-plus reduction in Q2 and Q3 shipments vs those achieved during Q4 2024 and Q1 2025 as a down cycle. The explanation may be elusive, and it may or may not be reversed by year end. But it is clear that the overall market activity is substantially lower globally. As is true of all past market shifts, Q3 contains substantial variations by product, geographic regions and mineral applications with some of the more notable ones outlined below. And a much more in-depth analysis will reveal differences if clients compare current distributions with those of past contractions.

Product lines: mining truck deliveries declined by 9% (units) and 11% (value) with the decline proportionately greater at the upper end of the size classes. Hydraulic shovels/excavators dropped by over 20%. And wheel loader deliveries declined by 17%, while their value dropped by a less severe 13% because units at the top end of the size categories held up to a greater degree. Dozers, both crawler and wheel, bucked this trend by increasing 9% in value.

Shipments to geographic areas diverged greatly as is often the case when contrasting quarterly shipments. Most of the decline was accounted for by Australasia and Russia/CIS. The two major country segments of Australasia declined but by much different degrees: Shipments to Australia declined by 21% but Indonesian miners and contractors accepted 58% fewer machines than in Q2. In sharp contrast to most countries, deliveries to Indonesia expanded between Q1 and Q2, but have now caught up to the declines in other countries and regions. Deliveries to Russia/CIS mines dropped another 32%. Mines in the region maintained their purchases in the two years after the war with Ukraine but have since fallen more than 50%. The impact of war-related export restrictions and financial limitations is likely to blame, but the long delay before these negative market factors is puzzling. Shipments in North America increased modestly (3%) while those to Latin America declined modestly (7%). And in contrast to these regions, Africa was up over 50%; Europe, Middle East (a relatively smaller market segment) expanded by 28%.

Mineral markets: Coal continued its long-term decline despite sustained coal production is several countries (India, Indonesia, Russia). Shipments to coal miners declined a further 35% Q2/Q1 totaling just $239MM; a remarkable decline from the nearly $1 billion quarterly average during 2022. Copper and gold miners increased their equipment purchases with copper shipments up 11% and gold up 19%. Although a smaller and geographically-concentrated sector, oil sands producers in Canada increased their deliveries by 19%. Deliveries to iron mines declined by 30% while those to other mineral miners declined by 10%.

After the substantial increase in shipments during the final quarter of 2024 and modest gains in the first quarter of 2025, the sharp decline in Q2 was surprising to Parker Bay and perhaps others who viewed the recent upward trend as sustainable and part of an expansion cycle. Instead, manufacturers’ unit shipments declined by nearly 15% with the aggregate value of these deliveries down a somewhat more modest 11%. Although U.S.-imposed tariffs and related trade negotiations/restrictions began at the start of the quarter and continued in complex fashion through the end of the quarter, we don’t consider these as having a major impact on mineral markets in general nor do we see deliveries as impacted by short-term adjustments to government-imposed exports/imports. And since equipment shipments are the end result of longer-term capital investment decisions followed by months-long purchasing decisions and subsequent manufacturing schedules, it seems unlikely that the decline in Q2 shipments resulted from the greater global market uncertainty that is impacting other economic sectors. All this said, the positive trend we observed after Q1 shipments is very uncertain.

As is true of all past market changes, Q2 contains substantial variations by product, geographic region and mineral application with some of the more notable ones outlined below. And a much more in-depth analysis will reveal differences if clients compare current distributions with those of both past growth cycles and contractions (should this be the start of one).

Product: The most noteworthy shift in quarterly shipments was the divergence of mining truck shipments vs. all other product lines: mining truck deliveries declined by $266 MM and -17% vs Q1. In sharp contrast, the combined value of all other products was essentially unchanged. The numbers of trucks delivered, and their value was marginally above the comparable measures during Q3 2024 – the nadir of the last contraction cycle. Manufacturers’ shipments of the three loading tools commonly paired with these largest trucks – hydraulic excavators, wheel loaders and electric/rope shovels – were valued at $500 MM in Q2, down just 1%. Within this group, hydraulic shovels/excavators account for more than two-thirds of the total and their numbers were unchanged, but down 4% in valuation owing to a modest downward shift in size classes. Wheel loaders delivered increased by more than 20%, but this was after very low deliveries in Q1. Although electric shovels declined, this product has represented a small and declining share of mines’ demand for the largest loading tools. Mining dozer deliveries are the third major class of machines covered by this analysis and their shipments were literally unchanged from Q1.

Geographic regions: As is almost always the case, changes in the geographic locations of mines, contractors and rental/lease entities (collectively) diverged substantially in Q2. Shipments to mines in Africa and Latin America were higher while those to other regions declined by 6% to 27%. Australasia, which accounts for 40% of global shipments, was down by 15% and this accounted for nearly 60% of the global contraction. Shipments to Indonesian mines accounted for virtually all of the region’s decline while in sharp contrast, Australian miners took in more machines than in Q1. North America declined by just 6% but deliveries to the mines in the region remain far below year-earlier levels. Russia/CIS mines continued to postpone purchases with Q2 shipments down 17% vs Q1, -28% vs Q2 2024, and less than half those of 2022-23. Imports have been largely cut off with war-related financing problems constraining mines’ capital spending.

Mineral markets: The often-mentioned decline to global coal markets continued in Q2 with shipments down 17%. While coal production in India, Indonesia and Russia sustained demand for large surface mining equipment, the population in other coal mining areas has contracted and, in some areas, transitioned to underground for coking coal. Shipments to the three major metals – copper, gold and iron – increased albeit modestly in Q2. Oil sands deliveries contracted by over 40% but the purchases and deliveries to the relatively few operations in Alberta oil sands swing sharply from one quarter to the next. Other minerals shipments increased by 8%.

Q1 Shipments: After the substantial increase in shipments during the final quarter of 2024, the less substantial 2% gain in the first quarter of 2025 is not surprising in our estimation. We see the modest 2% for both units and value as a continuation of a recovery and expansion cycle. If deliveries simply continue at the level of Q1 shipments ($2.4 billion), the full-year deliveries will provide manufacturers in aggregate, with the highest equipment revenues since 2012. Note: These valuations are very approximate and do not necessarily apply to individual manufacturers. Perhaps a better comparison is the number of machines delivered: 1,400; 25 more than the previous quarter, but still far below the nearly 2,000 shipped in Q1 2012.

As is true of all past market changes, Q1 contains substantial variations by product, geographic regions, and mineral application with some of the more notable outlined below. And a much more in-depth analysis will reveal difference if clients compare current distributions with those of the aforementioned 2012 peak.

Product: Truck shipments increased by 5% (units) but a more modest 3% in total value during Q1. The difference is accounted for by changes in the size-class mix: 90-110 payload units increased by over 12% along with a substantial increase in the 290- and larger ultra-classes. But these were largely offset by a 27% decline in the 218-255 class. Following a major increase in excavator shipments during Q4, unit deliveries increased another 12% while wheel loader shipments declined by 8%. The largest change during Q1 came in the dozer segment. The 168 units delivered was the fewest since Q4 2020. Parker Bay is unaware of any secular shift underlying this number and anticipates a return to the 200+ level in coming quarters.

Geographic regions: As is almost always the case, changes in the geographic locations of mines, contractors and rental/lease entities (collectively) diverged substantially in Q1. Shipments to Latin American operations increased by one-third, reversing the recent downward trend that had continued in Q4. Australasia shipments increased by 9%, primarily due to increases in deliveries to Indonesian mines. Indonesian shipments surpassed deliveries to Australian mines (essentially flat vs Q4) for the first time since Q1 2023. Offsetting these increase were declines in shipments to Africa (-17%), Asia (-29%), North America (-24%), and Russia/CIS (-13%).

Mineral markets: The secular decline in global coal mining requirements for equipment halted in Q1, but likely only temporarily. And it remains as the largest individual mineral segment. Gains were modest for copper (+4%) and iron (+5%) while shipments to gold mines declined by 12% despite strong market conditions and mineral prices for gold. This should be taken in the context of deliveries in the second half of 2024 which were higher that any half-year total since 2013. This reinforces our admonition that quarterly measures for both mineral groups and geographic regions must be taken in the context of longer-term demands.

The overall level of shipments reported by participating manufacturers increased by nearly 25% as measure in units and 14% by value. When Q3 showed a marked slowing in the rate of decline in shipments aggregates, we noted that it appeared the cyclical contraction was bottoming out. While one quarterly change may not represent the start of an expansion cycle, the magnitude of these latest numbers would indicate that is the case here. There was a small positive reading for Q1 2024 As measured by Parker Bay’s value- weighted Mobile Mining Equipment Index (2007 = 100), the Q4 2024 reading is 108.6 vs just 95.3 for Q3. There was a much smaller uptick for Q1 2024 shipments (+6%) but that was reversed through mid-year. Given the sharp increase in shipments, our index is now 5.5% short of the cyclical peak recorded in Q2 2023. And as measure year-over-year, the value of Q4 shipments – US$2.4 billion – brought full-year 2024 deliveries up to just 6% below 2023.

As is true of all past market changes, Q4 contains substantial variations by product, geographic regions, and mineral application with some of the more notable outlined below. And given that full-year measures are now available, key changes are also noted. But Parker Bay has not had sufficient time, nor do we have sufficient knowledge of all the underlying factors to understand the reasons for this strong increase in mining companies’ purchases in Q4.

Product: Mining trucks account for the majority of shipments and thus have the greatest impact on the total activity. Truck shipments increased by nearly one third vs. Q3 thus totaling nearly one thousand units for the first time since Q2 2023. The average size and value of these units was down substantially from Q3 but the increased volume was sufficient to improve aggregate value by 14%. Unit deliveries of hydraulic shovels/excavators reversed recent declines, increasing by nearly 50% while aggregate value rose by one-third vs Q3. But unlike trucks, these gains brought the market back to just 73% of the cyclical peak. It may be that given the longer lead times for the largest excavators, shipments will catch up with the trucks they are matched with over the remainder of 2025. Other excavating/loading equipment and dozers registered less dramatic changes but the Q4 improvements are significant for both wheel loaders and dozers.

Geographic regions: Changes in shipments to the seven geographic regions ranged from -18% to +78% (the latter being the relatively small Europe/Middle East). Australasia, which accounts for roughly one-third of all shipments and global population, increased by 35% Q/Q and reversed most of the nearly 30% decline that took place since Q1 2023. Latin American mines continued to take fewer machine shipments, valued at 6% less than Q3 2024 and more than one-fourth below the unusually strong Q1 2024 deliveries. African mine deliveries increased sharply but were far below the levels obtained in 2023. North American and Russia/CIS increased modestly, but for the former, they represented a 26% year-over-year increase, while for Russia/CIS the total was down 14% YoY.

Mineral markets: Machine shipments to coal mines increased 26% vs Q3 but less than half the level of quarterly shipment averages through Q3 2023. Copper and iron markets declined modestly while gold mine deliveries increased by more than 40% after declining by 25% during Q3. A more telling measure of the declining impact of the coal sector on equipment shipments is a comparison of 2024 shipments to a longer=term measure (2007-2023 combined). Over those years, coal accounted for a slight higher share of total shipments vs the three metal mines. In 2024, the three major metals represented 54% of all identifiable shipments vs 32% for coal mines (Note: Many shipments to contractors and rental companies are not initially identified by mineral mines where operated).

The overall level of shipments reported by participating manufacturers declined by just under 3% as measure in units and value. This continues to reflect a down cycle since Q2 2023. As measured by Parker Bay’s Mobile Mining Equipment Index (2007 = 100), the Q3 2024 reading is 96 vs 115 at the Q2 2023 peak for the last expansion phase. As is true of all past market changes, Q3 contains substantial variations by product, geographic regions, and mineral application with some of the more notable as follows.

Product: Mining trucks account for the majority of shipments and thus have the greatest impact on the total activity. Units delivered were down just 1.6% while their aggregate value increased by 5.6% reflecting the shift toward larger units with more than 250 delivered during Q3, a total greater than those delivered at the last cyclical peak. In contrast, unit deliveries of hydraulic shovels/excavators continued to decline by 19% vs Q2 (Q/Q) and nearly 30% year-to-date (YTD) vs the same period in 2023. As with the larger trucks they’re designed to load, the average size increased and Q/Q declines in $ valuation were substantially lower. This shift in average capacity carried over to wheel loaders with shipments declining 10% Q/Q while the value of these loaders increased by 4.3%. Shipments of dozers declined by 5% (units) and value (4%) on a quarterly basis taking the YTD measures down by 13%.

Geographic regions: Changes in shipments to the seven geographic regions ranged from -13% to +34% (the latter to the relatively small market for Asia). Australasia, which accounts for roughly one-third of all shipments and global population, declined by 6% Q/Q bringing the contraction since the region’s peak in 2022 to nearly one-forth. However, this contraction appears to have bottomed out in 2024. Latin American mines took delivery of machines valued at 13% less than Q2. But higher deliveries in the first half of 2024 resulted in an increase of 15% YTD. North America, one of only two regions to exhibit gains Q/Q, has now recorded the largest growth YTD — +31%. Mine in both Africa and Russia/CIS have declined sharply YTD. While we haven’t assessed the reasons for African mines, the contraction in Russia/CIS decline is most likely related to the impact of the war in Ukraine.

It now appears that mining equipment markets have bottomed out. But the impact of the recent election in the U.S. could affect global mining activity in ways that will be difficult to assess until changes in U.S. policies are more clearly defined.

In total, Q2 deliveries retraced much of the gains reported during Q1 as evidenced by Parker Bay’s Mobile Mining Equipment Index. The Index had fallen from a cyclical peak of 115 in Q2 2023 to just 95 in Q4 2023. While we had anticipated a continuation to begin 2024 (Q1 shipments increased by 14%, dollar-weighted basis), our preliminary reading of the index for Q2 shows the market falling back to 98 – only modestly above the Q4 2023 trough. As we’ve mention frequently, quarter over quarter changes are often erratic.

Shipments during Q2 were down 8.6% as measured by units delivered and 9.1% by valuation. More importantly, on a year-over-year basis, units delivered were down 23%, while the aggregate value of these machines was off a less substantial 14.6%; this reflecting higher unit-value hydraulic and electric shovels offset by greater declines in lower-value dozers and a modestly above average decline in mining truck deliveries. All of these numbers are subject to revisions as adjusts may be forthcoming from reporting manufacturers.

Underlying shifts continue within these totals: Latin America retracted much of the gains recorded in Q1 shipments. Australasia and Russia/CIS showed modest gains but on a year-over-year basis, both regions are down 20%+. African mines continued a year-long contraction with Q2 deliveries off 40% from a year-ago. North American mines took 5% fewer machines vs. the previous quarter, but they remain up 2% YoY.

Coal markets continue their secular and cyclical declines with shipments down 29% QoQ and a dramatic 56% lower than a year ago. Copper and gold continued stronger than other mineral markets, up a further 7.7% vs Q1. Iron markets lagged, though not nearly as much as coal. And oil sands surged to their highest levels since the start of 2023. This appears to be due in large part to their efforts to switch to autonomous drive equipment.

In contrast with the contraction in the second half of 2023, unit shipments in the first quarter of 2024 increased by nearly 10% (+119 units) while the aggregate value of these machines increased by more 16% from Q4, bringing this measure of market value to within 4% of the peak achieved in Q2 2023. We have often pointed out that quarterly data are somewhat erratic and cannot be relied on to measure market trends except over several quarterly reports. It now appears that the order of magnitude of the down cycle may be shorter and less severe. But we continue to anticipate market weakness in 2024 and our evaluation of other measures of market activities reinforce this assessment. But the degree to which Q1 shipments bounced back warrants substantial caution.

Within these aggregates, breaking down Q1 shipments point to some changes of note. Manufacturers’ shipments of large hydraulic shovels/excavators rebounded from a very weak Q4 with unit deliveries increasing by nearly 50% with a comparable increase in value. While the growth in truck deliveries was a more modest 7%, the mix was weighted toward the larger units such that aggregate value of mining truck deliveries increased by 14%. In contrast, deliveries of wheel loaders increased by one-fourth, but the value of these units was virtually unchanged reflecting a shift toward the smaller (20-mt payload) units. Crawler and wheel dozer shipments declined very modestly and this level of deliveries continued the decline in Q4 vs the previous two years’ (-14%).

Geographically, North and Latin American mines recorded extraordinary gains of 26% and 53%. For North America, this is the highest aggregate value of deliveries since 2012 and continues a resurgence in Q4 in the face of declines elsewhere. The increase among Latin America brought deliveries up to a ten-year high. Australasia and Africa, which had been relatively strong during the most recent expansion phase, both contracted modestly during Q1.

Q4 unit shipments were off by 20% with the aggregate value of those deliveries down by nearly 18%. This follows a more modest decline in Q3 vs Q2 and brings the total value of these machines back to the level achieved in Q2 2021 when the market began the latest growth cycle. This represents a nearly half billion dollar decline in US dollar terms for all represented manufacturers. Because the weaker second half of 2023 followed strong growth in the first, shipments were actually up 1.4% year-over-year with aggregate value greater by 6.5% due to higher values of the machines delivered (constant-dollar). The overall decline in global shipments is not spread evenly across products and especially geographic and mineral sectors:

Product lines: Mining trucks represent about 60% of the equipment population covered by the Database and they account for an only slightly smaller share of the contraction in Q4 shipments. The decline of 16% vs Q3 is sharp but less so than other product lines. Deliveries of wheel loaders, while a much smaller volume and value to the overall equipment market, held up quite well in the face of declining mine purchases, down just 7% in value vs Q3. Contrasting these two lines were hydraulic shovels/excavators – down 25%, and crawler and wheel dozers – off 26%. Although there may be long-term shifts in product distribution behind these most recent changes in production line, quarterly shipments are hardly sufficient to draw any conclusions.

Geographic Distribution: Most noteworthy is the sharp decline in for Russia/CIS which comprises roughly 16% of the global population and accounted for 29% of all deliveries in 2021 and 22% in 2022. Russia/CIS miners took delivery of machines valued at less than half of Q3 shipments and barely 30% of the peak levels achieved in Q1 2022. In contrast, North America was the only region with increased shipments: +16% vs Q3. While this is in line with the region’s share of the overall global population, North American miners have recently fallen far short of that share, accounting for just 7% of worldwide deliveries in 2021 and 10% in 2023. Although not nearly as pronounced as Russia/CIS, other regions experienced substantial drops vs Q3 lead by Australasia (-22%) and Latin America (-21%).

Mineral Markets: The overriding change to the mineral distribution of Q4 shipments is the decline in deliveries to coal mines – down US$336MM from Q3 and the lowest quarterly total since Q4 2020. This reduction in deliveries is attributed to the three countries that have represented the greatest share of deliveries during the previous three years: India, Indonesia and Russia. Deliveries to coal mines in these three countries accounted for 67% of all global coal mine deliveries over the past three years, and one-fourth of all global shipments during 2021-2023. In Q4, they accounted for less than half that share and almost all of the US$336MM decline in coal market shipments, down over 50% vs Q3. A couple other major mineral markets declined by substantial, but much smaller degrees compared to Q3 including a 17% drop in copper. While in contrast to these changes, gold mine deliveries increased by 35% and iron mines by 26%.

We recently noted some changes to segments of the global mining markets that might indicate the expansion phase was topping off despite there being no signs of a slowdown in equipment deliveries. The third quarter’s shipments may be signaling a downturn in the global market for new equipment. As we have cautioned in the past, a definitive trend can be confirmed only after a longer period, but reporting manufacturers delivered nearly 7% fewer units than in Q2 – 1,452 vs 1,560 with 10%+ declines in excavators, wheel loaders and dozers, and a slightly smaller drop in mining truck shipments. The collective reduction in valuation of these products was a more modest 3.2%. There were shifts in size-classes that accounted for much of this divergence between units and valuation. Within the truck market segment, gains in the larger size class, especially a 40% increase in 218-255 capacity units offset declines in deliveries with payloads under 150 mt. As a result, the value of truck shipments was marginally higher than that for Q2 truck deliveries. .

From a broader perspective, aggregate year-to-date deliveries are still 12% higher than those of the first three quarters of 2022 and full year deliveries are still expected to be higher than 2022. And it’s quite possible that Q4 markets could reverse this latest decline as happened in Q3 2022.

As is so often the case, regional and mineral segments shifts occurred yet again in Q3 with deliveries higher to mines in Africa, Asia, and Latin America, offset by lower shipments to Australasia, Russia and especially North America which were down over 20%. More meaningful measures are those comparing market segments’ share of shipments’ value for 2023 year-to-date with those for full-year 2022. There have been minor increases in geographic share for Africa, North America, and Europe/Middle East while Russia/CIS declined sharply from 22% of global shipments in 2022 to 17% thus far in 2023. While Parker Bay does not have sufficient underlying details, this decline is judged to be due to effects of the war in Ukraine both from the impact of export restrictions and possible declines in internal Russian economic activity.

Global shipments of machines covered in the Database reached their highest levels since the historical peak reached in 2011-2012 though remaining well below that expansion often dubbed the ‘Super Cycle’ for both mining and mining equipment markets. The 1,566 machines delivered is up over 10% vs. Q1 and 29% greater than year-ago shipments. Aggregate value of these machines increased by a more modest 8%. But this contrasts with Q1 when unit shipments declined marginally while valuations increased by 6%. Again this reflects shifts by product line and within product lines, by machine size. But overall, it’s clear that the mining equipment business remains strong. And at this point in time, we have no indications that there is a pending shift in this general direction. If the second half of 2023 show no growth but continues at Q2 levels, annual shipments will exceed 6,000 units, up 14% on 2022, with valuations totaling roughly US$10 billion, a level not achieved since 2012. And shipments could very well continue to increase in the second half.

As always, there are substantial changes among market segments by product line, geographic sectors and minerals produced. The most important or substantial include the following:

By product line: Mining truck deliveries (the dominant sector by volume and value) increased by 6% (units) and 7% (value). Other product lines were much more volatile. Following two substantial quarterly declines, crawler and wheel dozer shipments increased by more than 40%. High-value hydraulic excavators shipments surged in Q1 and then partially retraced those gains in Q2. But first half excavator shipments were the highest since the second half of 2012. Wheel loader shipments remain relatively weak, just +7% YoY.

Geographic distribution: Shipments growth in the Australasian region leveled off in Q2 after strong sustained growth since early 2021. Together Australia and Indonesia now account for more than one-third of global shipments. After weak equipment demand during 2022, Latin American mines were over 50% higher vs. Q1 and nearly as much YoY. North American shipments increased a more modest but substantial 17% over Q1 and nearly double the very weak second quarter of 2022. Deliveries to Russia/CIS mines leveled off in Q2 and appear to be headed for lower annual shipments vs. pre-war levels. Deliveries to Asian mines were strong while those to Europe, Middle East contracted by nearly one third. However the latter region is very small compared to others and thus the swings in shipments are often very substantial percentage-wise.

Mineral mines: Shifts in deliveries to mineral mines are particularly uncertain for Q2 because a very substantial percentage of shipments are not yet identified by mine (this includes contractor units, corporate-only identification, and deliveries identified by manufacturers only by country). For those with known mineral mine destinations, coal continues with the greatest share dominated by Indonesia and Australia with substantial deliveries to India and Russia. The three major metals – copper, gold, and iron – accounted for just over one-third; and all other minerals including oil sands represent around 10%. (Note: Parker Bay cautions against assessing short-term shifts in mineral market activity unless a larger percentage of global deliveries are identified by mine.)

Reported shipments for Q1 2023 continued to increase on a dollar weight basis by 6.7% while units delivered declined by 1.3%. This divergence derives from the changing distribution by product line and by size-class within those lines. Shipments of relatively lower-priced wheel loaders, dozers and drills declined, and truck shipments were off slightly. Offsetting all of these were high-value hydraulic shovels/excavators with unit deliveries up by more that 50% with aggregate valuation up nearly 70% owing to a surge in the largest units. It should be noted that these excavators experience frequent transitory shifts in deliveries given the small unit volume. For example, the value of their shipments declined by over 25% between Q1 and Q2 2022.

As always, these gains varied widely by mining region and mineral mined. Australasian deliveries were up 15%. While shipments were higher percentagewise for Asian (+36%) and Europe/Middle East markets, they are much smaller mining sectors with Australasia dominating the global gains in absolute terms. Russia/CIS deliveries continued to decline: -6% vs Q$ and a very substantial 36% decline vs Q1 2022. While specific reasons are unavailable to Parker Bay, it is most likely the result of trade restrictions and international financing constraints imposed by the war in Ukraine. Latin American markets were down nearly 12% following a trend through 2022 – puzzling result given the generally positive conditions in copper, iron, gold mining, all key sectors for Latin America. North American shipments were off 5% vs Q4 but his follows a surge across 2022 (+60% vs Q1 2022).

Deliveries to metal mines globally were strong in Q1: gold up 40%; iron +31%; and copper +19%. For all three markets, shipments declined across 2022. Shipments to coal mines were flat Q1 vs Q4 2022 and down nearly 30% vs Q1 2022. While coal is a very complex mineral sector, coal supply was generally higher in 2022 and prices for most subsectors declined by 50% or more. Not surprisingly, coal miners ratcheted back on new equipment deliveries. Shipments to oil sands were down substantially but much higher year-over-year.

Q4 2022 shipments data reported by participating manufacturers were surprisingly strong and this in spite of upward revisions to initially reported shipments for the first three quarters of the year. Participating manufacturers reported Q4 shipments of just over 1,500 units, collectively valued at $2.3 billion; this represents increases of 19% and 15% respectively over Q3. Even more impressive are the gains recorded on an annual basis. With Q4 up sharply along with previous 2022 quarters that compared favorably to year-earlier ones, 2022 as a whole saw shipments of nearly 5,294 units vs just over 4,000 in 2021 – a gain of 26%. The estimated $8.6 billion value of these 2022 shipments compares to just under $7 billion for last year’s deliveries — +23%.

We recently noted that both new and used equipment markets were ‘tight’ with indications of higher and perhaps escalating prices and extended delivery lead times. The latest figures reinforce this and our observation that equipment markets were expected to remain strong at least into early 2023. With forecasts of a global recession being tempered, miners might not ratchet back on capital spending and shipments may hold or even increase over the already strong Q4 levels.

Shipments during Q3 as reported by participating manufacturers were +3.5% (units) and +1.4% (valuation) higher than Q2. Because of the strong gains recorded in late-2021/early-2022, Q3 2022 deliveries were still up significantly over year-ago numbers: units delivered were up nearly 16% and value of shipments a somewhat smaller 12.3% YoY. There were no substantive shifts between product lines within the quarterly totals except for wheel loader shipments which dropped 18%. Trucks were up 6%, dozers 4%, and hydraulic shovels/excavators dead even.

Geographic shifts are common quarter to quarter and the most recent one was no exception. African mines reversed much of the Q2 increase as did miners in Asia. Despite hosting some of the biggest copper, gold and iron mines, Latin America recorded a fourth consecutive drop in shipments which are now 43% below a year ago. Australasia recovered from a modest Q2 decline with Q3 deliveries up 17% QoQ and +69% over the year ago level, primarily thanks to strong deliveries to Indonesia. North American miners recorded only a modest gain vs. Q2 but are now up 58% vs. a year ago.

Despite the significant decline in iron ore prices, miners took delivery of machines with valuations up a collective 72% vs Q2, but modestly lower than Q3 2021. The only other mineral market higher in Q3 vs Q2 was coal (+22%). Again, there were underlying regional shifts which over time are transforming the coal industry away from several traditional markets (U.S. Canada, South Africa) and toward Russia, India and Indonesia. Copper remains somewhat enigmatic: despite the consensus of being critical to several growth sectors, global copper consumption was up just 4% in 2021 and the increase in 2022 is expected to be somewhat lower in 2022. Deliveries to the largest copper mines were down 18% vs Q2 and more than 20% vs year-ago. Parker Bay doesn’t expect these negative comparisons to continue long-term. While equipment demand from gold mines worldwide has been essentially flat vs Q2, it is down nearly 40% vs Q3 2021. Oil sands shipments have been very erratic recently in part owing to the much smaller number of mines and attendant equipment fleets. We do anticipate future growth due in part to the much higher oil prices and part due to mines’ stated plans to upgrade existing truck fleets to autonomous drive.

The total number of machines reported shipped by participating manufacturers increased marginally in Q2 (+20 / +1.7%) but the mix shifted to smaller, lower value products such that Q2 deliveries declined by just over US$150 MM or -7.4% VS. Q1. Mining trucks, which account for the majority of both units and value, declined by 6% with a mix weighted toward the lower end of the size-class range. Units with payloads of 220-mt and greater declined by nearly 30% while widely utilized 90-110 mt units increased modestly. Hydraulic shovel/excavator deliveries were down 10% (units) with aggregate value declining nearly 20% due to a substantial drop in units with rated payloads of 40-mt+. Offsetting these declines was a 50%+ increase in crawler and wheel dozer shipments. But this only served to partially reverse the 40% decline in Q1 dozer shipments.

Geographically, the most significant change was for mines in Russia/CIS. The region has surged for several years with deliveries second only to Australasia during the expansion that began in Q4 2020. But in Q2, that changed dramatically with shipments down over 30%, mostly likely reflecting a myriad of economic dislocations brought on by the war in Ukraine and accompanying sanctions placed on Russia by many of its heretofore trading partners. Shipments to Australasian mines likewise declined but by a more modest 15% and this followed a very strong Q1 (+33% QoQ). Australian mining markets remain strong, but they could falter if China’s supply chain problems and other economic disruptions continue and impact imports. Latin America was the third region to decline in Q2 but by a more modest 10%. The other four regions showed increases in quarterly shipments with Africa and Asia up by more than 50% following very weak Q1 totals. North American mines took deliveries of machines valued at 9% more than in Q1 and exhibited a 30%+ gain over year-ago deliveries.

The increase in Q1 shipments decelerated from the very strong gains achieved in the second half of 2021 especially Q4. This is reflected in Parker Bay’s Mobile Mining Equipment Index (Q1 2007 = 100) which increased to 95.3 from Q4’s 93.0. Unit volume declined slightly while the value of these machines increased by a modest 2.4% as compared to the 16% increase recorded by Q4 2021 deliveries. This reflects in part a shift among product lines – shipments of higher priced hydraulic shovels/excavators and trucks increased while deliveries of relatively lower-priced wheel loaders and dozers declined. Within product lines, deliveries of hydraulic machines were on average substantially larger but not the mining trucks they are paired with. Such discrepancies are not likely to reflect long-term pairings as they represent only a very small percentage of the operating population of both. The decline in both dozer and wheel loader shipments have been protracted and substantial. Since the most recent expansion cycle began in Q4 2020, unit shipments of trucks and excavators are up 170% and 73% respectively (albeit from very depressed levels in Q3 2020). But dozer deliveries are still 6% below the start of the expansion; wheel loaders nearly 20%. Sales of both product lines held up better during the last contraction. And part of the explanation may be due to the availability of good quality used machines which in general are more easily resold and transferred than larger machines. But it is not yet clear to Parker Bay if there are other contributing factors to the continued weak shipments of these two product lines.

As is very often the case, quarterly shipments vary widely by geographic region and mineral application. These variations were particularly wide in Q1 2022. Geographically, the more traditional markets with the largest equipment requirements – North America and Australasia – were up 21% and 34% respectively, while Latin America, Africa and Asia all declined by 16% or more. Deliveries to Russia/CIS mines declined by 7% but it’s questionable whether this was the result of the war in Ukraine. It affected only the last six weeks of the quarter and likely had no impact on shipments within Russia/CIS or China. Mineral markets diverged greatly with iron mines taking on 77% more shipments than in Q4 2021 and Canadian oils sands more than tripling from a very low Q4 2021, yet only +5% YoY. Shipments to coal markets worldwide increased by a modest 7%. In sharp contrast, the previously strong copper and gold sectors declined by more than 30% each. Again, we caution reading too much into changes from one quarter to the next.

Although growth in shipments decelerated from Q4, the conditions for continued gains remain in place, at least in the short term. Mineral prices are generally strong and output higher and growing. In some markets there are indications of supply shortages. Although Parker Bay does not have access to manufacturers’ orders and backlogs except as they are made public, there are indications that they continue to grow, and that delivery lead times are longer than a year ago. One manufacturer cited increased utilization of machines in service, and this should indicate that miners will require additions to their fleets if demand for their output continues to grow. And used equipment sales are reportedly strong. All these conditions point toward continued growth.

But there are also problems that will limit these gains. Manufacturers’ costs are increasing, and they are understood to be passing this increase along in higher prices. There are continuing supply chain problems, and these may worsen as the impact of the war in Ukraine expands. It now appears there will be no near-term settlement of the hostilities. Based on public disclosures, indications are that some Ukraine mines have remained in operation while those close to the Black Sea have been forced to suspend operations. Machines at those operations are recorded as ‘parked’ and account for about 20% of the national total. But it’s possible that operations at other mines have been disrupted, resulting in larger numbers of inactive equipment than reported in the Database.

Outside of Ukraine, the Database does not yet reflect significant impacts of the war. Some sectors, both mining and mining equipment, will undoubtedly be affected even after a hoped-for settlement of hostilities. Russia exports of coal will be affected though not to all countries. U.S. manufacturers have suspended activities in Russia and sanctions will limit sales from North American and European equipment suppliers. These will likely be replaced by Russian/CIS equipment suppliers and, perhaps, by imports increased from China. All of these changes and more may be part of greater shifts in trade patterns and economic dislocations. Coupled with monetary authorities’ efforts to contain inflation, the result could well be a global recession which would likely result in mineral and mining market contractions and declining equipment sales later in the year or in 2023. But for now, we expect some continued growth in machine shipments this year.

After substantial declines in the global market for large mobile surface mining equipment during 2019-2020 (in part Covid-related), strong gains were recording across 2021 despite some supply-chain problems. During the fourth quarter of 2021, shipments increased by 16% over the third quarter of the year and a very impressive 43% over the fourth quarter of 2020. For the full year, 2021 shipments topped US$7 billion for the first time since 2018. Parker Bay’s Surface Mining Equipment Index (constant dollar-weight, Q1 2007 = 100) increased from 79.5 in Q3 to 92.3 in Q4 while remaining well below peak level obtained in 2012-13.

Deliveries by product line, geographic region and mineral sector were generally though not universally higher. Mining trucks accounted for the majority of 2021 shipments’ value at $4.5 billion which derived from deliveries of nearly 2,700 units. Hydraulic shovels/excavators were second in shipments value at just over $1 billion followed by crawler and wheel dozers at $830 million.

Even on a year-over-year basis, the differences between regions were stark. Russia/CIS shipments more than doubled and accounted for nearly 30% of all 2021 shipments value at $2 billion. Australasian shipments nearly doubled and accounted for just under $2 billion. Deliveries to Latin American mines increased by 37% over 2020 resulting in total value of $1.2 billion. The fourth largest region, North America, saw shipments decline by 5% when compared to full-year 2020. A similar decline of 3% was recorded for African miners.

General mining market activity does not appear to have changed materially over the past three months. A few mineral markets where prices had surged to record or nearly record levels (copper, gold, iron, met coal) have pulled back but not necessarily enough to discourage mining companies from continuing with equipment replacement and expansion plans. The explanation of the moderating shipments activity may at least partially lie with global supply chain problems that have affected virtually all sectors of the global economy. Given the long lead times for some of the essential components in mining equipment manufacture, these problems may have begun earlier in the year and are only now being manifested in product deliveries. One major manufacturer has publicly stated that Q3 shipments would have been higher if not for “supply chain snags” and that they expected these to continue into 2022. While we’re not privy to other possible manufacturers’ supply chain difficulties, it’s likely that many of them were impacted in a similar fashion as many equipment suppliers depend on some of the same component suppliers.

Comparing Q3 2021 to Q3 2020 shows markedly better numbers. Q3 2020 was the cyclical bottom and thus the year-over-year data accumulates the previous three quarters’ gains producing a 57% favorable increase over that cyclical bottom. But as indicated by Parker Bay’s index, the mining equipment markets remain well below the peak achieved at the end of the mining super-cycle of 2012.

Within the aggregate Q3 shipments totals are the usual variations: mining truck deliveries were marginally higher, dozers slightly lower. Within this and other product lines, shipments by size-class diverge but are quite likely to reverse during the next or subsequent quarters. Hydraulic shovels/excavators bounced back part way from the significant Q2 decline (+18% after -33% Q2/Q1). As we’ve often noted, secular changes are only evident over several years.

Q2 continued to reflect general mining market improvement but with some unusual divergences that may simply reflect quarterly rebalancing of manufacturing and delivery activities among the several major suppliers. They may also be indicative of mines’ priorities among equipment types as they continue to restock following the contraction that ended in Q3 2020. Our index of equipment shipments (based on estimated value of shipments and indexed to 2007 = 100) was 71 for Q2, up just 4% above Q1 but a more robust 27% YoY. This latter gauge will likely record even more positive growth for Q3 shipments as the comparison will then be with the Q3 2020 bottom. The index remains nearly one-fourth below the previous cyclical peak (Q4 2018) representing a gauge of how far manufacturers have to return to that previous level of production. In summary, the current growth phase of the equipment business cycle appears to be on-track but not as growth-oriented as we expected at this early stage of recovery/expansion following the Q3 2020 cyclical bottom.

As indicated by our index, there was a 23% increase in unit volume but just 4% in estimated value of shipments. The explanation derives chiefly from the product mix and, to a limited extent, shift in size classes within each product line. The numbers of lower-value dozers and wheel loaders were up 63% and 50% Q/Q but each around 25% Y/Y. Unit trucks shipments were up 13% Q/Q but just 3% in value. We expect this to balance in the second half with more of the large (220 mt+) trucks being delivered based on large orders placed during the past 12 months. And despite the modest gains in Q2, truck shipments were the highest in two years. Deliveries of the very high-value excavators and shovels declined by 29% Q/Q and nearly 40% in the value of these shipments. We expect this product category to bounce back in the second half of 2021 to better match the levels of truck shipments.

Gains in shipments to mines in Australasia, Africa, North America, and Russia/CIS were offset by a sharp decline in deliveries to Latin America, Asia and Europe/Middle East with the greatest impact stemming from Latin America. As we have noted in the past, quarterly shipments by region can be highly variable and, in particular, we don’t expect the low level of demand from Latin American mines to continue.

Parker Bay continues to expect strong growth during the second half of 2021 based on:

As always, there is uncertainty and impediments to growth, e.g., government and non-government objections and limitation to new mine development. But there does appear to be continuing mitigation of the adverse effects of the pandemic. So our assessment is that the positive factors will outweigh the negative for the balance of 2021 and into next year.

Shipments during the first three months of 2021 slowed from the rapid pace recorded in the last quarter of 2020. The number of machines delivered was essentially level while the value of these shipments increased by 6.3% (due to changes in product mix and size-classes within products). Thus Parker Bay’s Surface Mining Equipment Index (value-weight with Q1 2007 = 100) rose to 68.4, the highest since Q3 2019. In contrast, unit deliveries increased by 12.9% YoY while value of shipments were higher by just 7.6% compared to Q1 2020, pointing out once again that quarterly variations can often be quite irregular. Taken in this context, the market expansion appears to be continuing albeit at a slower pace. But we would expect to see higher growth during the balance of the year especially in light of strong mineral market dynamics and a presumed global economic recovery from the pandemic-induced contraction.

Shifts among products were even more pronounced than usual. Unit shipments of hydraulic shovel/excavators were up more than a third; trucks by 15%. In sharp contrast, crawler and wheel dozer deliveries were down by one fourth and wheel loaders by over 35%. Shifts within each product line are even less reliable indicators of long-term trends. Average truck capacity was little changed Q1 2021/Q4 2020 but large gains were recorded at both ends of the size range with both 90-mt payload units and ultra-class units showing the greatest gains.

Geographically, shipments growth accelerated in Latin America to the highest level in seven years while gains in Australasia represented a mere rebound from the Q4 level which was the weakest in four years. Shipments to African mines, which typically swing up and down, decreased by nearly 20% as did North American deliveries. Deliveries to mines in Russia/CIS continued the Q4 recovery after very weak sales during the first three quarters of last year.

The total number of machines delivered during Q4 2020 increased by 35% while the value of these machines was 26% higher than Q3. This is a substantial break from the contraction that began in Q1 2019 and which brought equipment markets down more than 40% over the seven quarters ending with Q3 2020. Parker Bay’s Mining Equipment Index (Q1 2007 = 100) peaked during the last expansion cycle at 92.7, then declined to 50.7. This index increased to 63.7 indicating the global market may have experienced an inflection point with sustained and substantial growth possible in 2021 and beyond. It’s an understatement to suggest there may be ‘headwinds’ as the global economy and mineral markets continue to deal with the pandemic and it’s impact on every facet of life. But a recovery in mining equipment markets does appear to be underway.

Manufacturers produced and delivered (761) machines during Q4, up from just (562) in Q3. This brought the annual total to just over 2,600; nearly one-third below the 2019 total. The value of Q4 shipments totaled US$1.4 billion vs US$1.1 billion for Q3. For the year, shipments barely topped US$5 billion, a 25% decline over 2019. And for reference, during the peak of the SuperCycle that ended in 2012, annual shipments topped US$14 billion.

Overall, it appears markets are recovering but it should be noted that this is a single quarterly gain, albeit a strong one. Should global economies continue to recover despite the adverse constraints imposed by the virus pandemic, the mining sector is expected to improve through 2021 and beyond. And along with it, mining equipment markets are expected to show significant gains. How significant is an open question.

The number of machines delivered in Q3 declined by 7.7% from Q2 shipments while value of these delivered dropped by 7.2%, reflecting a modest shift toward higher-value equipment as well as shifts toward larger-scale units within the product lines. But these changes are generally insignificant. On a year-over-year basis the decline was just over one-third (units) and 30% (value). And from the peak of the last cycle the declines were 48% and 45%. Given the ongoing economic and mining industry turmoil brought on by the pandemic, it’s difficult to assert the industry has reached a cyclical ‘bottom’ but it does appear the contraction is softening over the past two quarters.

Underlying these overall figures are some very substantial variations by product, mineral and geographic sectors. Truck and dozer shipments were down double-digits Q/Q with truck deliveries off nearly 40% YoY. In sharp contrast, hydraulic excavators were up more than 40% from Q2 while wheel loaders were essentially flat. Excavator deliveries have been very volatile in 2020, declining by nearly half between Q1 and Q2, then recovering most of that loss in Q3. Similar shifts are evident in the geographic numbers. Substantial declines occurred in most regions: Africa -22% (measured in value), Latin America -17%, North America -19%, Russia/CIS -30%. Shipments to Australasian mines increased by a modest 5% while deliveries to Asian mines were up 24% and those to Europe/Middle East gained over 40%. But worthy of note, the latter two regions are substantially smaller in overall size than the others.

Changes to shipments by mineral shift dramatically quarter by quarter and Q3 was no exception. Despite generally unfavorable long-term prospects, coal remains the largest sector with over 20% of the value of all Q3 shipments. While this was essentially unchanged from Q2, it represents a 44% drop from Q3 2019. Gold mines recorded a 43% decline Q3/Q2 but were +26% YoY reflecting very strong pricing. Copper was up 9% but sharply lower YoY. In contrast, iron mining deliveries were down by one fourth Q3/Q2 but up modestly YoY. Shipments to oil sands mining (a substantially smaller and geographically more concentrated sector) have been extremely volatile but in general decline (-50% YoY) reflecting pandemic induced declines in oil demand and attendant oil pricing.

Q2 deliveries totaled 637 units and with an aggregate value of US$1.23 billion. This represents a decline of just 6% in units and 11% in $ value – less than Parker Bay expected given the severe, virus-driven closures and declines in many other business sectors. It’s worth noting that these equipment markets had already weakened substantially over the previous five calendar quarters such that Q2 total units were down 47% and market value 40% from shipment levels at the end of 2018. With the unique worldwide economic conditions within which miners and equipment manufacturers are operating, it is extremely difficult to determine whether current levels represent a bottom for the contraction cycle that began at the end of 2018. But we do estimate that deliveries are now below long-term replacement requirements. And postponing such replacement of economically and physically obsolete units can only be delayed for a relatively short time if mine production is to be maintained.

The value of shipments (measured in recently depreciated US dollars) declined more than units because of shifts between and within product lines. High-value hydraulic shovels/excavators declined by 42%. And while truck deliveries were down just 5%, units in the ultra-class segment (290-mt+ payload) declined by 26%. Offsetting their reduced shipments was an increase in dozer deliveries (+19%). Analogous to trucks, wheel loader unit volume was up 2% while value declined 5% reflecting growth in the smaller (20-mt payload) units. Oftentimes these differences are reversed in subsequent quarters. When compared to levels reached at the peak of the last expansion cycle in Q4 2018, equipment shipments are down substantially for all product lines with the exception of low-volume electric shovels (+67%).

Geographically and by mineral, the changes in shipments varied widely on a quarter-over-quarter basis with Africa up 47% and all other regions down to varying degrees: 1% for Russia/CIS while North and Latin American mines each declined by more than 30%. Deliveries to coal, copper and other minerals declined Qtr/Qtr while shipments to gold, iron and oil sands all increased. Other than our usual caveat that short-term shipments do not necessarily represent longer-term shifts in market shares, we would suggest that declining global prospects for utility coal demand is translating into greatly reduced equipment requirements which is reflected in both the latest and recent measures.

Mining equipment shipments declined during Q1 2020 but at a slower rate than recorded during the second half of last year. Although these deliveries were made in the face of the ongoing virus pandemic, it is unclear how significant the global health crisis and accompanying economic contraction was on shipments that were underway when the mining industry began coping with the virus spread during the first months of 2020. This impact will undoubtedly become more substantial during Q2 and the balance of the year. Furthermore, industry capex and ordering of large new production equipment began a significant contraction during the middle of 2019 with the factors driving this current down cycle only exacerbated by the mining sector’s response.

Units delivered declined by 7.5% vs. Q4 2019 while the estimated value of these deliveries was less than 1% below that of the previous quarter. After reaching a plateau 9 to 18 months ago, shipments have retraced approximately half of the gains recorded during the 2016-2019 expansion cycle. While further declines can be expected, they might not be as severe as other measures of mining sector and general business activity that is widely expected as the world copes with the pandemic’s economic impact.

The decline in Q1 deliveries was uneven across product lines with mining trucks declining while shipments of hydraulic shovels increased, wheel loaders and electric/cable shovels were unchanged and dozers declined modestly. Average size of those truck shipments increased. As in the past, all these shipment numbers are subject to minor additions and adjustments as manufacturers’ refine their initial accounting (these have been insignificant in recent reporting). And quarter-to-quarter changes by product, geographic and mineral sectors may not represent longer-term market shifts.

Equipment markets continued the contraction that started in Q1 2019 and accelerated during the second half of the year. During the fourth quarter, global shipments declined by an additional 11% (units) and the value of these deliveries dropped by an estimated US$150 million (down 9% vs Q3). On a year-over year basis, unit shipments in 2019 were 18% lower than during 2018 while total estimated value declined by 12%. The latter reflects a continued shift toward larger/higher-value products and, within product lines, larger size classes.

The quarterly decline was due almost entirely to a reduction in mining truck deliveries which were off 16% vs Q3. Shipments of excavating equipment (hydraulic shovels/excavators, wheel loaders, electric/rope shovels) and dozers were virtually unchanged. This is in sharp contrast to the decline recorded during Q3 when shipments for these product lines accounted for a substantial share of the overall reduction in equipment deliveries.

There was a wide divergence in equipment deliveries among geographic regions with sharp reversals of changes recorded during Q3. Whereas shipments to North and Latin American mines increased Q3 over Q2 (vs. sharp contractions for other regions), they declined sharply during Q4 while shipments to Asia and Russia/CIS increased modestly. The distribution by mineral markets likewise exhibited wide divergence. Copper – down 53%; oil sands down 28%; coal down 2%; gold up 49%; iron up 8%. As Parker Bay has noted in the past, changes in quarterly shipments are often not reflective of longer-term shifts in product/geographic/mineral markets.

Possible revised reports by participating manufacturers plus additions for non-participating manufacturers will likely raise the current shipment totals. But experience indicates such changes are likely to be minor (1-4%). And these will almost certainly not change the fact that equipment markets declined substantially during 2019 albeit not nearly as severely as during the first year of the 2013-2015 contraction.

Just 835 machines were delivered during Q3 — a 24% decline vs. Q2. The value of these shipments was 17% lower than Q2 reflecting disproportionately greater reductions in the delivery of lower-priced product lines and smaller units within those product lines. While this marks the third quarterly decline this year, it is far greater than those recorded in Q1 and Q2 which appeared to be more of a pause in the latest expansion cycle. It appears to mark the end of the recovery/expansion that began in Q2 2016 but the severity of the decline is disproportionate to conditions in other mining activity.

The declines are widespread but mask substantial variations by product line, size, geography and mineral with some sectors increasing while others dropped even more sharply than the overall contraction. Shipments of mining trucks (by far the largest product line in terms of both units and value) were down by 25%; excavators/loaders by 22% with hydraulic shovels/loaders leading the decline. Crawler and wheel dozer shipments were down by 14%. In sharp contrast, electric/rope shovel deliveries tripled but the volume for these extremely large excavators is very small.

Geographically, the changes during Q3 reflect a reversal of the strength in several regions while ones that lagged behind during the expansion to date increased during Q3. Shipments to mines in Russia/CIS decline by over 40%; those in Australasia by 27% (with a much larger drop in deliveries to Indonesia). In contrast, North American shipments increased by 14%; Latin American deliveries by 24%. This ‘rotation’ among sectors was anticipated, but not the severity of the declines.

Similarly a ‘rotation’ in mineral sectors seems to be developing if Q3 shifts continue. Shipments to coal miners in India, Indonesia and Russia — which led the expansion over the past 2+ years – declined sharply in Q3 with global shipments to coal mines off by 37%, accompanied by reductions in deliveries to oil sands (-10%) and gold (-8%). However, copper mine deliveries were up 58% and iron +13%.

As we’ve often noted, quarter to quarter shipments, especially when broken down by product, size-class, geography and mineral, do not always represent longer-term trends. But it is hard to categorize the substantial decline in Q3 shipments as a glitch. It is possible that subsequent revisions to manufacturers’ shipments will raise currently reported levels but these typically amount to single-digit revisions. And it is possible that short-term order placements or manufacturers’ inventory adjustments had a disproportionate impact on reported shipments that will be reversed in Q4. It is also possible that the contraction will continue for the balance of 2019 and into 2020. But Parker Bay does NOT anticipate any contraction to be of the intensity or duration of the one experienced during 2013-2016.

Activity in the large mining equipment sector has clearly leveled off during the first half of 2019 after three years of recovery and expansion. In our opinion, it’s not clear yet whether this represents the beginning of a market contraction or simply a pause in a longer-run growth cycle. Mineral output levels and pricing are not moving in unison and are impacted by both general economic trends (e.g., the trade dispute between China and the U.S.) and events impacting individual sectors (e.g., the impact of the tragic tailings dam failure in Brazil). And with production/delivery lead times for many of the products covered in the Database, it’s difficult to determine how these factors impact shipments data calendar quarter to quarter.

Nevertheless, the data for Q2, along with similar results for Q1, point to an inflection point versus the positive trend that began in Q2 2016. This is reflected in Parker Bay’s Large Mining Equipment Index which declined by one percent (Q2/Q1) and now stands at 88.5 (2007 = 100). This index is value-weighted utilizing a constant-U.S. dollar price. And it masks significant shifts by product, mineral and geography.

Although the value of shipments declined by just one percent, units shipped dropped by nearly 8%. Deliveries of higher-value excavating/loading equipment increased appreciably: hydraulic shovels/excavators by 22%, wheel loaders by 17%. Offsetting these was 23% decline in crawler and wheel dozer deliveries which had increased by more than one-third between Q3 2018 and Q1 2019. Mining truck shipments, which account for the majority of machines shipped, declined by more than 5%; but only 1% on a value-weighted basis as strong growth in deliveries of ultra-class trucks helped balance declines across the smaller classes.

First quarter 2019 mining equipment deliveries indicate a marked slowing in the volume of shipments and a 5% decline in the value (the latter being our rough estimate based on approximate prices by product/size-class). In total, unit deliveries were up by just five machines vs. Q4 2018 (+0.4%). At the same time, Q1 shipments were more than 10% higher than Q1 2018. And it should be remembered that further reporting and refinement of these shipments frequently results in minor upward revision (+1% to +5%). But even if such adjustments materialize, the Q1 will represent a decided leveling off of the growth the industry has experienced since mid-2016. Whether this is the beginning of a sustained contraction or just a ‘pause’ in the current contraction will depend on both internal mining market dynamics as well as global economic and political developments.

As is usually the case, this overall change in shipments masks more significant shifts by product, geography and mineral. Mining truck shipments, which account for the lion’s share of the total, increased by just five machines, but this total was 5% lower than Q1 2018. Hydraulic shovel/excavator delivers decline by 26%. While the number of units in this product category is small relative to mining trucks, average value/price of these machines is much higher. And the accounts for almost the entire decline in the industry’s total shipments value for Q1. Crawler and wheel dozers shipments continue to increase sharply: +14% vs. Q1 and +88% vs. Q1 2018. While difficult to measure, we believe this growth is due in large part to the much lower availability of ‘late model’ dozers in the used equipment markets. Other product line shipments were relatively unchanged.

Geographically, deliveries to mines and contractors in Russia/CIS and Australasia maintained the strong positions they established in 2018 but shipments to Australasia decline both absolutely and as a share of the global total while shipments to Russia/CIS increase. North American mines accounted for a 14% share of Q1 vs. just 10% for all of 2018. Latin American and African deliveries declined while shipments to Asian mines increased.

With respect to shipments by mineral market, coal continued as the primary sector accounting for more than 50% of shipments. Copper and iron mines maintained their relative shares but shipments to gold mines declined substantially. The latter may reflect major gold miners’ focus several major mergers and, if so, major capex commitments for these machines may resume in the year ahead as management assesses their new asset bases post-merger.

Globally, a total of 1,221 units were delivered in Q4 2018. This represents only a 1% increase over the revised Q3 total but more than 30% vs. Q4 2017. However, the value of Q4 shipments increased by a more substantial 5.6% over Q3 as miners shifted some capex to larger-scale equipment, something that has lagged during the recovery/expansion to date.

It should also be noted that on average, quarterly reports have been revised upward by ~5% recently. For example, total 2017 shipments were originally reported at 3,285 but they now total 3,399. But even if Q4 2018 figures are revised upward, it appears evident that growth in equipment demand and subsequent shipments has been slowing now for three quarters. This may not signal a downturn and there are factors that could drive demand significantly higher. But optimism for 2019 should be tempered by other factors including projections of slowing global economic growth and the potential impact on mineral demand from international trade disputes.

Total Q3 mining equipment unit shipments decreased by about 1% vs. Q2. But significant changes in the product mix toward larger, higher-value machines resulted in a four percent gain in the value of these shipments to more than US$1.8 billion. Changes from quarter to quarter often reflect short-term factors and may not persist going forward. Looking back over a longer period – Q3 2018 vs 2017 – the gains are far more substantial: +29% in units and +22% in value.

The first noteworthy difference in Q3 data is in the product mix: excavating and loading equipment, deliveries of which have lagged those of the trucks they are matched with during the recovery and expansion cycle, increase by 21% while trucks increased by just 7%. In sharp contrast, crawler and wheel dozers declined by 28% after nearly doubling across the previous three reporting periods. Hence the decrease in volume but increase in overall value.

Geographically, the very rapid growth in shipments to mines in Russia/CIS was sharply reversed in Q3 with total deliveries down 29% and falling below year-ago levels. Nevertheless, shipments to Russian miners remained second only to Indonesia among national markets. Indonesia continued the surprisingly strong gains in shipments propelled by continuing growth in coal markets and the contractors that support this mining sector. Australia also contributed to the Q3 growth in Australasia with the region accounting 40% of the global value of these products. Significant (though lesser) gains were recorded by North and Latin American mines. Among the smaller mining regions, Asia and Europe, Middle East markets gained while deliveries to African mines declined. Given the smaller size of these regions, quarter-to-quarter changes may not reflect longer-term trends.

Changes in the mineral distribution continued the trend away from coal, but coal mines collectively remained the largest buyers during Q3 with Indonesian and Russian mines accounting for over 70% of shipments to coal mining. Among the other major mineral markets, deliveries to copper and iron mines continued to increase and represented a combined 32% of the value of Q3 shipments vs. just 26% during Q2. These deliveries were dominated by Latin American copper mines whilst iron mining shipments were split more evenly among mines in Australia, Brazil and to a lesser degree North America and Russia/CIS. Shipments to oil sands increased while deliveries to gold mines declined. All these mineral market shares should be considered preliminary as a significant number of machines have not been identified by mineral (as yet).

Parker Bay considers this slowing of the current expansion cycle a ‘pause’ rather than foreshadowing a downturn. The gains recorded among larger miners reflect increasing capex both for sustaining existing production and some initial increases to that existing capacity.

This latest report marks two full years of growth since markets bottomed out in Q2 2016. Since then, deliveries have tripled yet remain well below the peak level achieved in 2012. Compared to Q1 2018, unit shipments are up 7% and 33% year-over-year. The value of shipments is estimated to have been virtually unchanged over the past three months. The divergence of units and value stems largely from the product mix with most Q2 increases recorded for smaller dozers, drills and graders. In contrast, truck deliveries (which account for the majority of units and value shipped) increases by less than 1%. Hydraulic shovels/excavators increased by 27%; crawler and wheel dozers = 37%, motor graders = 42%; drills = 83%. Wheel loaders and electric/rope shovels declined and continue to lag behind the other product lines during the current expansion cycle.